14 August 2022 • 2 minute read

The FCA's new consumer duty: shifting the mindset

The Financial Conduct Authority (FCA) has now published its final rules and guidance on its new Consumer Duty (PS22/9 and FG22/5). The Consumer Duty is designed to fundamentally shift the mindset of firms in how they deliver for consumers.

The implementation of the Consumer Duty is a flagship initiative for the FCA, setting out its expectations of the industry over the next years. The FCA is requiring the industry to put the customer at the heart of what they do and to be able to demonstrate how they are achieving good outcomes for customers. The FCA has made clear that it will have a key role in successfully embedding the duty, by making it central to its Supervision, Authorisation and Enforcement strategies. Firms should expect progress against the implementation timeline to be at the forefront of many of their interactions with the FCA.

The Consumer Duty will apply to all firms in the distribution chain for products and services sold to retail customers.

The Consumer Duty will apply to: (1) all new products and services from 31 July 2023; and (2) closed products and services from 31 July 2024 – which will require firms to undertake a review of their backbook.

Overview of the Consumer Duty

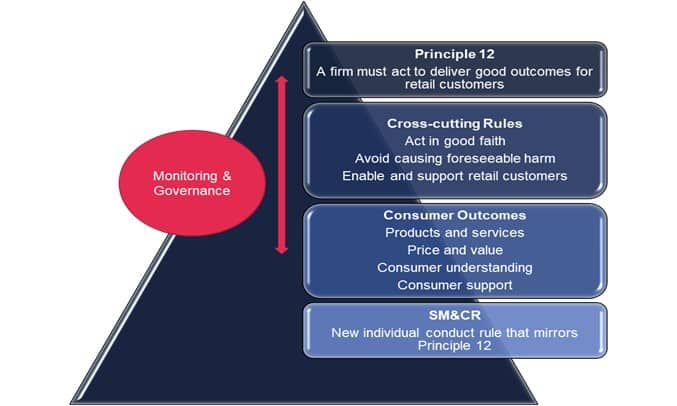

A new Principle 12 will require firms to act to deliver good outcomes for retail customers.

The three cross-cutting rules clarify the FCA’s expectations under Principle 12.

The four consumer outcomes represent the key elements of the firm-consumer relationship, which are instrumental in helping to drive good outcomes.

This is underpinned by new requirements on governance and culture and monitoring of consumer outcomes.

The FCA has also introduced a new individual Conduct Rule 6 for staff to act to deliver good outcomes for retail customers.