19 December 2023 • 8 minute read

PepsiCo Decision - Landmark judgement regarding the application of Royalty Withholding Tax and Diverted Profits Tax

In a significant decision on 30 November, 2023, Moshinsky J of the Federal Court held that certain payments made in relation to Bottling Agreements were royalties and thus subject to royalty withholding tax or in the alternative, that diverted profits tax would apply. The ATO was successful in arguing that certain portions of the payments related to the sale of beverage concentrate were royalties and thus subject to royal withholding tax limited to 5% under the US/Australia double tax agreement.

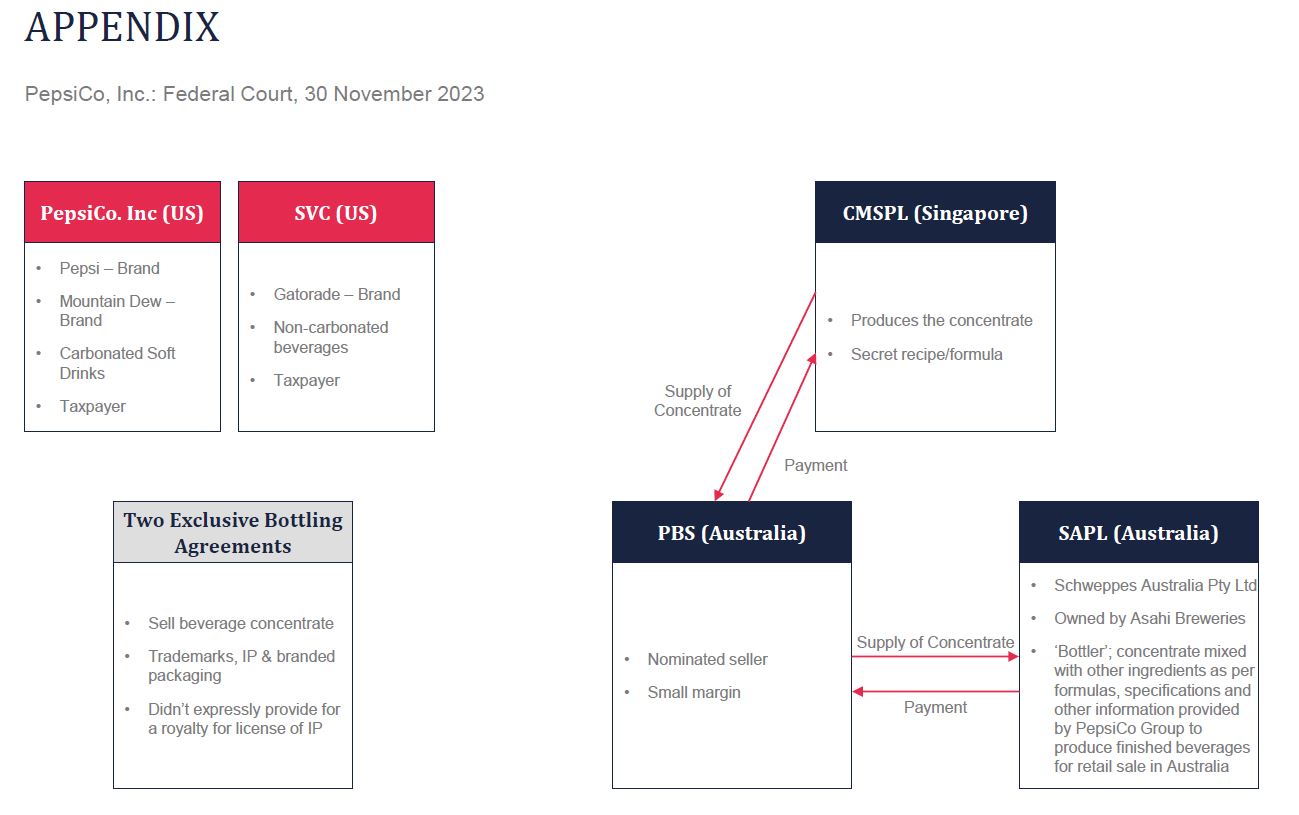

Under the two exclusive Bottling Agreements involving PepsiCo, Inc. (PepsiCo) and Stokely-Van Camp, Inc (SVC), two US resident companies, Schweppes Australia Pty Ltd (SAPL), an Australian resident company, was effectively provided with the beverage concentrate to produce finished beverages for retail sale in Australia, as well as, an express or implied license of trademarks and other intellectual property (including brands) covering both carbonated soft drinks (eg. Pepsi and Mountain Dew) and non-carbonated beverages (eg. Gatorade).

Please find below a structure diagram which sets out the relevant parties, their roles and the supply of concentrate and related money flows. It is important to note that the beverage concentrate was produced by a Singapore based associate of PepsiCo and that the sale of the beverage concentrate to SAPL could be made by either PepsiCo, SVC or a nominated seller.

Royalties & Royalty Withholding Tax

The court held that certain portions of the payments made under of the Bottling Agreements were royalties as defined in Section 6(1) of the 1936 Tax Act as well as Article 12(4) of the US/Australia Double Tax Agreement; noting that the relevant definitions of royalties include amounts paid however described (or computed), or payments or credits “of any kind”.

In particular, the court said that it was important to consider the terms of the relevant agreements in their "business and commercial context". The court in principle determined that the relevant royalty component was 5.88% of SAPL’s net revenues from sales (subject to further revision/adjustment). ie. relating to the use of, or right to use the relevant trademarks and other intellectual property.

While the payments on their face were for the purchase of beverage concentrate, this was not determinative of their characterisation for purposes of the domestic Australian or US/Australia Treaty definitions of “royalties”.

The case involved payments with respect to the years of income ended 30 June, 2018 and 2019.

Amongst other things the court highlighted the following:

- The purported seller of the beverage concentrate to SAPL, ie. PepsiCo Beverage Singapore Pty. Ltd. (PBS Australia), was not a party to the Bottling Agreements ie. only a nominated seller.

- Each of the Bottling Agreements contained a license by either PepsiCo or SVC (as applicable) of the relevant trademarks and other intellectual property to SAPL; in the case of PepsiCo it was an implied license and in the case of SVC the license was an express license.

- In each circumstance, the license of the trademarks and other intellectual property was fundamental to the agreement, in the sense that without the license, SAPL would not have agreed to make the payments.

- The payments by SAPL were intrinsically linked to the license of the trademarks and other IP; noting that one of the witnesses for PepsiCo in giving evidence during cross examination stated that he was not aware of the sale of PepsiCo concentrate ever being offered without a license of the brand – they "always go together".

- Although the SVC license was described as “royalty free”, the court held that this was not determinative of the proper characterisation of the payments.

- Although the Bottling Agreements nominated PBS Australia as the seller of the concentrate to SAPL, this constituted a direction to SAPL to pay PBS Australia, rather than Pepsico or SVC. However, as a matter of contract under the Bottling Agreements and the fact that PepsiCo and SVC were the parties to the Bottling Agreements, SAPL’s payment obligations were owed to these two US companies. Accordingly, Pepsico and SVC were "beneficially entitled" to the relevant portions of the payments under Article 12 of the US/Australia Treaty.

- Accordingly, the relevant portions of the payments were properly regarded as paid to PepsiCo or SVC under Australia’s domestic withholding tax provision which extends to payments "otherwise dealt with on behalf of the other person or as the other person directs".

Diverted Profits Tax (DPT)

Although the court said it was unnecessary to consider the application of Diverted Profits Tax because of the conclusion on royalty withholding tax, it did in principle hold that Diverted Profits Tax would otherwise apply.

Briefly, the Diverted Profits Tax (DPT) was introduced in 2017 and the PepsiCo decision is the first Australian Court decision on the application of the DPT. In essence, the DPT can apply where the taxpayer has obtained a DPT tax benefit in connection with a scheme and it would be concluded that one of the persons who entered the scheme did so for the principal purpose of enabling the taxpayer or another taxpayer to obtain a tax benefit, or both to obtain a tax benefit and reduce foreign tax liabilities. Subject to certain carveouts, the relevant taxpayer must be a "significant global entity" and where applicable, the Commissioner can apply a 40% tax on the amount of the diverted profits.

The principal issues in the decision related to the alternative postulate or counterfactual. Firstly, the Commissioner argued that one counterfactual would be as follows; ie. that the relevant Bottling Agreement might reasonably be expected to have expressed that the payments to be made by SAPL be for all of the property (including the trademarks and other IP) provided by the PepsiCo Group Companies (rather than the concentrate only). This approach was essentially adopted by the Court.

Further, the Court found that the relevant schemes would achieve a reduction in US tax for PepsiCo and SVC which was critical to the tax benefit analysis.

Finally, the Court concluded that one of the principal purposes of each of PepsiCo and SVC in entering into the relevant scheme was to obtain a tax benefit (namely not to be liable to pay Australian Royalty Withholding Tax) and to reduce foreign tax (namely US tax on their respective incomes). The Court said that both Bottling Agreements were contrived in that the payments were ostensibly for beverage concentrate alone, whereas in substance they were both for concentrate and the license of valuable IP.

Similar ATO disputes and activities

It is important to note that there are other similar disputes emerging with the ATO relating to similar arrangements affecting beverage concentrate, branding, trademarks and other intellectual property including an important case involving the Coca-Cola Company, Coca-Cola Amatil and related entities, as well as other sector reviews/enquiries related to royalty free licenses or more broadly applicable payments for "embedded" royalties for the sale of goods and/or services.

Key Takeaways – broader ramifications

While the decision deals with the very specific circumstances of the sale of beverage concentrate, bottling arrangements and related intellectual property including trademarks, branded packaging and similar arrangements, on one view, the PepsiCo decision was very much decided on its particular facts and agreements/documentation in these circumstances. In this context, the decision highlights the broader characterisation of the relevant payments (including the use of, or the right to use IP) and most importantly, that it is necessary to consider the terms of the relevant agreements in their "business and commercial context". Further, the decision deals with the circumstances involving an express royalty free license or implied license, and arguably in principle is not directly relevant to a broader range of circumstances, particular other sectors.

Clearly, the PepsiCo decision will likely have wide-ranging implications for the access to and use of, intellectual property across a broad range of sectors and on ATO rulings dealing with royalties and related matters, including the licensing/distribution of software and DEMPE of intangibles.

Thus, it is likely that the outcome of this decision may have an immediate impact on the ATO’s draft ruling (TR 2021/D4) which sets out the ATO’s views on the characterisation and tax treatment of certain receipts from the distribution and licensing of software. This draft ruling was expected to be finalised in January 2024.

Further, the ATO in its Media Release of 1 December, 2023, amongst other things, points to broader applications of the PepsiCo decision including as follows:

“The Tax Avoidance Taskforce has for a number of years been targeting arrangements where Royalty Withholding Tax has not been paid because payments have been mischaracterised, particularly payments for the use of intangible assets, such as trademarks.”

The ATO also refers to its Taxpayer Alert 2018/2 on embedded royalties and it indicates that the decision “sends strong signals to other businesses that have similar arrangements to review and consider their tax outcomes”.

Other sectors with highly valuable IP including the Consumer Goods/Retail and Pharmaceuticals/Medical/Life Sciences sectors, are likely to be impacted by the decision.

The decision also confirms that the DPT can now be a real tool in the ATO’s arsenal to tackle multinational tax avoidance and profit shifting. The strong focus of the DPT on the "commercial and economic substance" as distinct from the "legal form or shape" of commercial arrangements will be increasingly important.